US

US

UK

UK

Credit Cards vs. Charge Cards: Which One Is Best for Your Business?

According to a recent survey, 79% of small businesses have found it difficult to access affordable capital. Yet, 75% of small business owners (SBOs) remain optimistic about their financial trajectory in 2024.

For these SBOs, the right financial tools are crucial for managing cash flow and driving growth. Business credit cards and charge cards are two popular options, each with unique features, benefits, and eligibility requirements.

Understanding the pros and cons of each can help small business owners choose the best option to access the capital they need to grow their business.

What is a business credit card?

A business credit card is issued to a corporation rather than an individual. This means the business, not the owner, is responsible for charges made with the card. Business credit cards are typically issued to companies that demonstrate financial stability, have an established business credit history, and meet specific requirements set by the lending institution.

What do you need to qualify for a business credit card?

- Proven track record of profitability

- Established credit history

- Registered as a C-Corp, S-Corp, or LLC

- Strong business and/or personal credit score

| Pros of business credit cards: | Cons of business credit cards: |

| No personal liability for business owners | Stringent eligibility requirements to qualify |

| Spending controls and expense management | Potential for misuse can lead to excessive spending |

| Enhanced business analytics | Annual fees which can add up across multiple cards |

| Rewards programs such as airline miles, hotel points, and cash back | Potential to negatively impact a company’s credit score |

| Elimination of employee reimbursement processes | Limited legal protections for unauthorized use or fraud |

| Interest and late fees can increase the overall cost of borrowing |

What is a charge card for a business?

A business charge card allows a company to make purchases and pay for them later, avoiding interest charges but imposing penalties for late payments. These cards often do not have a preset spending limit, however, they do require the balance to be paid in full each month.

| Pros of charge cards: | Cons of charge cards: |

| No interest charges if the balance is paid in full each month | Fewer issuers compared to credit or debit cards |

| Higher monthly spending limits offer enhanced flexibility | Full balance repayment requirement |

| Avoid accumulating debt, encourage responsible spending | Requires strong financial discipline |

| Builds business credit and offers rewards programs | Often carry annual fees |

| Legal protections for unauthorized use or fraud |

Which one is right for your small business?

Credit cards:

- Suitable for larger businesses with consistent and growing revenue

- Ideal for companies needing to issue multiple employee cards and utilize advanced expense management tools

- Some corporate credit cards may require a personal guarantee from business owners

Charge cards:

- Best for businesses with steady monthly profits and disciplined spending

- Beneficial for avoiding interest charges and promoting financial responsibility

- Require full monthly balance repayment, making them less suitable for businesses with unpredictable cash flow

Select the right financial tool for your business

Choosing between a credit card and a charge card depends on your business size, financial stability, and spending habits. Credit cards offer extensive benefits and tools for larger businesses, while charge cards can be a valuable tool for small businesses with consistent revenue streams.

Your smart small business growth solution

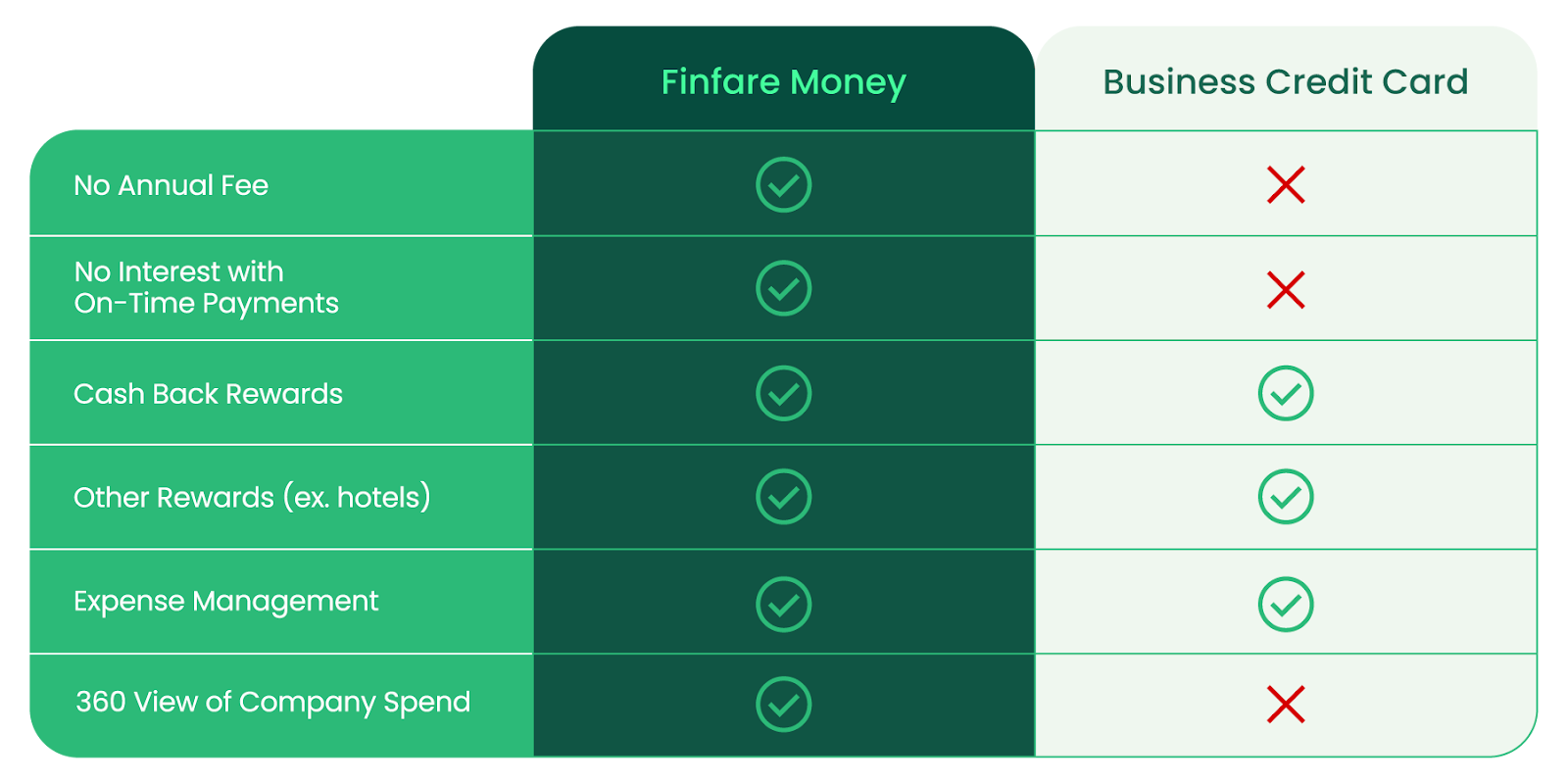

Finfare Money gives small businesses a better way to access capital for monthly expenses, manage spending, and earn generous cashback rewards—all within a single, easy-to-use solution. Plus, as your business grows, you may qualify for expanding your available credit.

- Business charge cards with monthly credit: Finfare Business Charge Cards are connected to a business credit account, providing flexible, secure, and controllable ways to make business purchases.

- 360° view of your company spend: Whether it’s your credit, your cards, or your spend—you can manage your entire account from our included expense management tool.

- Cashback and other rewards: From 1.5% or more cash back* to additional rewards and discounts, Finfare gives you the most options for making money on purchases.

- No personal guarantee or credit check required: You can apply for business credit without a personal guarantee or personal credit check—your available credit is based on your business history.

- Issue physical or virtual cards to your team: Physical and virtual cards create flexible, secure, and controllable ways for you and your team to make purchases, with spend limits and merchant controls.

- No fees for on-time payments every month: Unlike standard credit cards—with Finfare Business Charge Cards, there are no fees and no interest, so you can spend smarter on what matters most.

- Purchasing power and savings—plus QuickBooks integration: Connect your QuickBooks to streamline and simplify accounting, knocking one more item off your to-do list!

Ready to grow your business with Finfare Money?

*Cashback available on Qualified Purchases only. See Terms for details. Cash back in excess of 1.5% is dependent on individual merchants and offers through the Mastercard Easy Savings™ program.

Easy Savings™ gives you access to various merchants offers which may include cashback or instant discounts. Visit www.priceless.com/easy-savings for details.

The Finfare Executive Charge Card is issued by Cross River Bank, Member FDIC, pursuant to a license from Mastercard. This is not a deposit product.

The Mastercard circles design is a registered trademark of Mastercard International Incorporated.